A Critique of Mark Zuckerberg Comments To Joe Rogan and The Financial Analysis-Based Case For Diversity in Corporate Environments

Madison and Wall: Saturday Summary for January 18, 2025

Each week on the M&W Podcast, we discuss Madison & Wall’s latest research. Last week we introduced our Advertising 101 series, a multi-part (i.e. every week all year long) tutorial that will explain how the industry really works and why money flows as it does.

We kicked things off last week with Gerry D’Angelo (formerly the global VP of media at Procter & Gamble) and talked about how marketers organize themselves. This week our guest is J. Francisco Escobar, President & Founder of JFE International Consultants, one of the industry’s foremost experts on marketing procurement. In this episode we explore how and why the marketing procurement function sets so many of the frameworks that define the decisions that marketers make with respect to their media and advertising activities. As much as anything we have done to date, we guarantee this series will be worth your while.

It’s now available on Spotify, Apple, or wherever you get your podcasts.

We have also recently launched the Agency Business podcast focused on the business of agencies in collaboration with Olivia Morley’s FusionFront Media. In our newest episode, Olivia Morley and I are joined by Joanne Davis, one of the industry’s leading agency search consultants. In this episode we talk about the impact of AI on fees (and related emerging functions such as prompt engineers and creative lawyers), whether clients get the agencies they deserve, how important agency culture is to marketers and much more. Click here to listen now.

Weekly work

This past week we provided an extensive critique of Meta CEO Mark Zuckerberg’s comments made on The Joe Rogan experience on January 10, especially about diversity in corporate environments. Beyond highlighting some apparent oversights (our recollection was that Meta’s mostly male management team prior to 2007 wasn’t particularly commercially successful, and that it wasn’t until Sheryl Sandberg joined that it became a real business) we provide a financial analysis-based argument for diversity

We published our analysis of new economic data with read-throughs for the advertising industry this year in context of all of the political uncertainties ahead

We participated in two public webinars to discuss the current state of the advertising industry. On Wednesday we were on the IAB’s US Ad Spend Outlook hosted by Chris Bruderle and on Thursday we appeared with Deborah Wahl on a live event hosted by Mediaocean’s Aaron Goldman to discuss their new 2025 Outlook Report, a survey of more than 700 marketers’ views of plans for the year ahead.

More Context

There was a significant amount of press coverage over the past week in relation to an interview Meta’s CEO Mark Zuckerberg participated in with Joe Rogan on The Joe Rogan Experience.

Most notably, Zuckerberg made comments about a “culturally neutered” and “emasculated” society along with the positive benefits of “masculine energy” in a corporate setting. Although the full interview did convey that Zuckerberg believes that both “feminine” and “masculine” energy are desirable and that “you want women to be able to succeed,” we thought the general direction of his argument was particularly ironic because Meta’s commercial successes were arguably largely due to Sheryl Sandberg, the company’s COO from 2008 to 2022. Prior to that time, when the company had massive consumer scale but no meaningful commercial model to speak of, the senior management of the company was comprised entirely of male executives as far as we can recall.

When paired with the company’s other announcements in past two weeks (not only the elimination of third party fact checking, which will undoubtedly lead to the presence of more hateful content directed towards non-white males on Meta platforms, but also the termination of DEI programs), Meta is harming how it is perceived among larger marketers much as was the case between 2017 and 2020. During that era, Facebook and Instagram were platforms that many larger advertisers bought only begrudgingly, making that spending less assured than it could have been. Of course, large agency-served marketers only represent a modest share of spending – we think marketers who work with the six largest holdcos probably only account for ~20% of Meta’s revenue - so we are mindful that any negative sentiment towards Meta has limited consequences. By the time many large brands engaged in a widespread boycott during 2020, in the wake of then-President Trump’s “when the looting starts the shooting starts” post, growth in spending from other smaller obscured any negative consequences in Meta’s financial results.

More generally, the comments made on Rogan’s podcast can be contextualized alongside the broader economy-wide roll-back of DEI initiatives in the face of activist pressure and political change. If it wasn’t clear before, many corporate DEI advocates were only ever fair-weather supporters rather than true believers in the advantages of diversity over any potential costs.

Our view as analysts is that diversity actually matters to the long-term health of businesses, less because of any moralistic perspective and more because of our studies of finance and corporate decision-making.

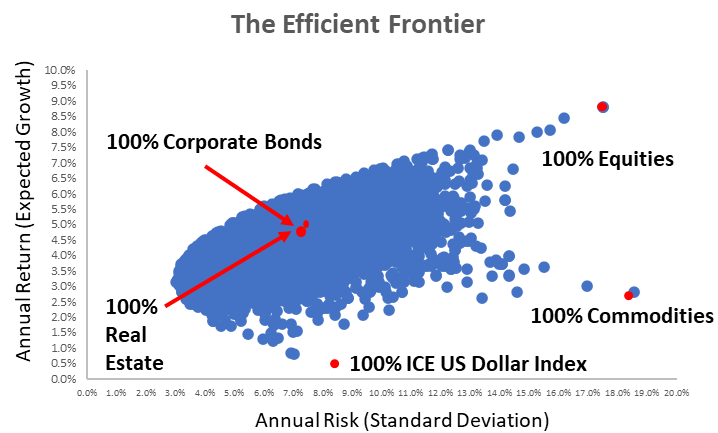

The financial view is based upon the well-studied benefits of diversification in capital markets. The concept of the “efficient frontier” is that because individual asset classes are not overly correlated with each other, the most desirable portfolios of asset classes for any given risk tolerance can be found on the top boundary of the hyperbola that captures every possible combination of asset classes measured in terms of each portfolio’s expected risk and return.

In a well-designed, efficient portfolio, the "ups and downs" of assets will balance each other out if the assets are indeed uncorrelated. In essence, when the forces of the market are pushing a certain class of asset down, there are contrarians in the mix that help to limit the damage and vice versa. Overall, as the math underpinning the efficient frontier concept proves out, the outcome of diversification is generally superior risk-adjusted returns.

In this metaphor, a CEO is like an asset class. We think that when they surround themselves with like-minded people or people with similar backgrounds (or worse, “yes-men”), it’s not unlike holding a concentrated portfolio. In the case of Equities we can see how returns have been higher, but then so too are risks vs. almost any other combination of assets. Even worse, some portfolios (or CEOs) are like Commodities where returns are relatively low and risks are even higher. Almost any diversification will produce a superior overall portfolio.

Put differently, when the forces of industry are pushing companies to move in one direction, a contrarian voice in the room – whether informed by a difference of background or experiences – can help avoid potential disasters.

Financial theory insists that the diversified portfolio will outperform a concentrated portfolio (with the exception of outliers). Below we can see what the risks and returns for 10,000 different combinations of portfolios and individual asset classes were using data from 1999 to 2023.

Source: Madison and Wall. Real Estate based upon Case-Schiller US National Home Price Index, Commodities based upon Bloomberg Commodities Index, Equities based upon SPX and Corporate Bonds based upon Bank of America Corporate Bond Index, all for periods from 1999-2023.

The read-through for us is very clear: while quality still matters greatly, with that held constant, diversity produces superior risk-adjusted returns whether in investing or the assembly of management teams.

Concurrently, when we see management teams at companies who are not particularly diverse, our past experience studying corporate decision-making strongly suggests that those management teams are in place less because of those individuals’ merits and more because of the personal relationships they have previously established. In general, the presence of less-diverse teams leads us to question whether or not more senior decision-makers actually looked for the best people to fill jobs or whether they simply relied upon people who they know from within their personal networks (which will generally be less diverse than society is as a whole). To be sure, it’s possible that the “best” people for certain unique situations might all have monolithic backgrounds, but it’s highly unlikely that this would hold when it comes to operating large corporate entities.

Overall, the presence or absence of diversity has an impact on how we think about individual companies’ long-term prospects relative to a company’s peers. On balance, given the logic and the math outlined above, we think that longer-term outcomes for more diverse companies will be relatively more positive when compared with less-diverse ones. To the extent that Meta finds ways to ensure they maintain diversity despite everything described above, we would predict they will be better off than if they become less diverse as an organization. However, without specific policies to encourage diversity across the business, it seems less likely that this will occur.