Amazon Prime Video Ad-Free: No Change To Long-Term Challenges for Ad-Supported TV

Amazon announced that starting in early 2024, Prime Video will start including “limited advertisements” with an ad-free upgrade option (for content other than live sports) for an additional $2.99 per month in the US, and with different prices elsewhere.

Given the initial positioning of many of the biggest streaming services as ad-free subscription video on demand offerings, I’ve written and spoken extensively about the consequences of a world where consumers are increasingly watching TV free of ads, and the challenges for advertisers in managing reach and frequency against broadly defined audiences in this world. To the extent that formerly ad-free services increasingly have ad-supported options available to consumers, what will the consequences be for advertisers?

In general, I think it doesn’t have a huge impact on my basic thesis, that the capacity of television to support reach-based marketing goals is increasingly compromised with every passing year.

Here’s why.

While a service that defaults all consumers to ad-supported viewing will undoubtedly end up with providing more reach than one which doesn’t, I am persuaded by the idea that when given the option, most consumers will pay for ad-free experiences if they are consuming a lot of a service.

In other words, perhaps by the end of 2024 only a quarter of Prime Video subscribers might pay up for the ad-free upgrade, but I bet these will be the heaviest consumers of the service, such that substantially more than a quarter of viewing will be ad-free. I think the same will be true for every other service, such that the less intense a consumer’s relationship with a service, the more likely they will stay on an ad-supported tier, so long as they maintain their subscription. I’ve not seen data to support these assertions so still keep an open mind in this particular instance.

However, one thing I feel more strongly about – supported in part by data – is that in general consumers have a higher-than-expected tolerance for effective price increases to support ad avoidance.

For a first illustration, consider the rise of the DVR in the 2000s. As I recall it, it was the heaviest consumers of TV who were most likely to pay extra for what had become a monthly service fee from cable operators. True, the on-demand aspect of DVRs was important, but so too was skipping ads on the most desirable content.

For a second, consider what’s been happening to consumer spending on video services. While there are many observers who have opined that consumers are dropping or are likely to drop their streaming services as prices rise, whether for ad-free or ad-supported offerings, total spending on streaming services is consistently rising. I argue that at least in the US this can occur for a significant period of time because there is a large pool of existing spending available to fund it without causing total video expenditures to go up by much: traditional pay TV. With approximately $100 billion spent on these services last year, down from a peak of around $110 billion in 2017 on my estimates, ongoing high single digit declines in pay TV penetration free up significant resources. By comparison, spending on streaming services as aggregated by DEG amounted to “only” $35 billion last year.

Source: Madison and Wall, DEG, Box Office Mojo

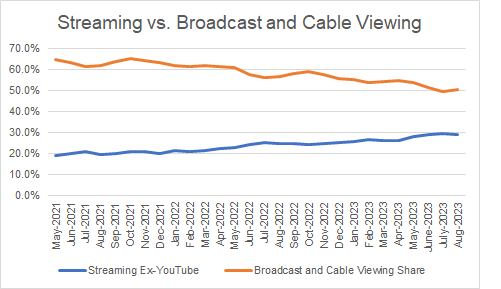

If we oversimplified and considered the ratio of viewing of streaming to traditional TV as reflected in Nielsen’s The Gauge– put YouTube and “other” viewing aside for the moment - streaming amounts to 58% of the viewing on broadcast and cable. There is clearly a significant time-value gap between these two.

Source: Madison and Wall analysis of Nielsen data

I don’t doubt that there will be an increase in the number of people who could be reached by ads with Amazon’s news vs. a world where Amazon didn’t offer an ad-supported version, and that’s certainly a positive for Amazon and for the existing eco-system, at least on the margins. However, I remain doubtful that the news meaningfully alters the industry’s long-term trajectory. Advertisers who depend on television to support their marketing goals will need to significantly refine the ways they define and make use of ad-supported television inventory in their campaigns as a result.