Disney FY4Q23/CY3Q23 Results: Ad Trends Better Than Peers; Industry-wide US Pay TV Subs Fall 7%

Beginning in January 2024, most Madison and Wall research and related data published on this Substack will primarily be available to consulting or advisory clients, or otherwise as part of a paid corporate subscription. Please reach out to brian@madisonandwall.com if you would like to discuss these services or for more information about the new offering.

Disney reported its fiscal fourth quarter 2023 results covering the calendar third quarter of the year on Wednesday. Although specific company-wide advertising results were not disclosed – typically, more complete details of the company’s advertising results from its fiscal fourth quarter are not published until the day before Thanksgiving – advertising at the network and local stations were down was down on viewing trends and the absence of political advertising. DTC segment revenues included negative advertising results at Hulu which likely wouldn’t have offset the introduction of advertising to Disney+ nor growing ad revenue at Disney+ Hotstar. Meanwhile, domestic ESPN ad revenues were positive

Ad-supported subscribers to Disney+ grew 2 million to 5.2 million and 50% of new US subscribers (implicitly gross additions, which were undisclosed) chose ad-supported option. During the prior quarter, company management stated that 40% of all new Disney+ subscribers chose an ad-supported option. Ad-supported subscribers launched outside of North America on Nov. 1, so implicitly the vast majority of the 5.2 million ad-supported subscribers are in the US. The company had 46.5 million total subscribers to Disney+ in North America at the end of the most recent quarter.

In commenting on the broader market, CEO Bob Iger stated that “overall, advertising has improved…while it's not as strong as we would like it to be, it's certainly not as bad as some people think it is, and it's working for us.” Indeed, towards these ends, if a few of the industry’s biggest TV network owners were slightly down to slightly positive on the quarter (Disney, Fox and Univision), a couple were down mid- to high-single digits (NBC Universal and Paramount) and one was down by double digits (Warner Bros. Discovery) then total national TV, including various forms of connected TV was probably down by around 5% year-over-the-year, which would represent an improvement from prior quarters rates of declines, although aided by easier comparables from the year-ago period.

Anecdotally, retail media may be one of the bigger indirect contributors to declines in national TV at this point in time, as the largest marketers who need to fund their retail media budgets don’t have many other “traditional” sources from which to fund this spending beyond television. Although Amazon remains the biggest player in this space – and they haven’t even begun to meaningfully attack television budgets as they will with the launch of the ad-supported version of Prime Video – Instacart is another player in the space, and coincidentally on Wednesday afternoon they also reported results. For their third quarter, ad revenue rose by 19% year-over-year.

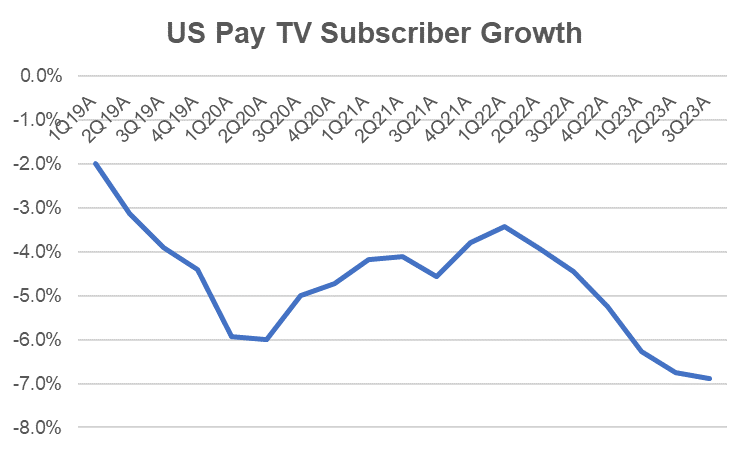

Bigger challenges for television remain. With the disclosure of Hulu Live’s subscriber gains — now at 4.6 million at the end of the third quarter, vs. 4.4 million one year ago, making it the country’s sixth largest distributor of all TV networks — we now have about as much data as will be published by significant vMVPDs. While DirecTV does not disclose its subscribers in its current corporate form, if trends impacting fellow satellite TV company DISH are impacting DirecTV in a broadly similar manner, total pay TV subscriptions – including cable, satellite and virtual MVPDs – in the US probably accelerated slightly in the quarter, with an approximate 7% year-over-year decline. Assuming this pace of decline doesn’t accelerate, there would be approximately 69 million households with pay TV services by the end of next year, which would compare to what should be around 135 million households at that point in time.

Source: Madison and Wall, company reports

With this context, increasingly direct discussion about the inevitability of the availability of the flagship ESPN – whether owned as it presently is (80% Disney and 20% Hearst) or in a different form – as a DTC service was also a topic on the earnings call. While the availability of a DTC version of ESPN could contribute to accelerated declines in conventional pay TV subscriptions, it’s very possible that making it available in this form could still be a net positive for subscription revenues.

It’s important to consider from here that if ESPN becomes primarily available to subscribers who pay for it a la carte, then presumably this would mean fewer casual fans would watch ESPN’s programming, reducing the relative value of the network as an advertising vehicle. On the other hand, if ESPN programming were still broader reaching than alternative sources of professional video-based content in whatever aggregated form of distribution it might take, it could still fare almost as well in the future as an advertising platform as it does now.