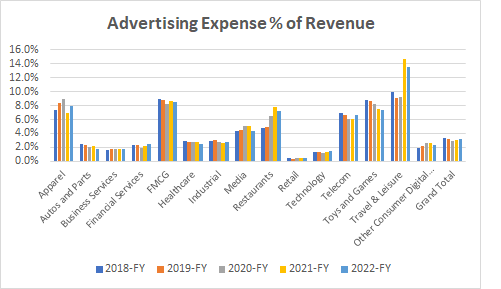

Do Ad Budgets Correlate With Marketer Profit Margins? Not Really

Source: Madison and Wall analysis of data for selected companies as aggregated by Refinitiv.

I’ve been curious about the relationship between profit margins of large marketers and the degree to which they may determine advertising budgets. Looking at a group of 87 of the world’s largest marketers for whom I could use Refinitiv to aggregate consistent profit margin and advertising expense data back to 2013 on a continuous basis, I calculated the change in profit margins and the change in the advertising expense ratio (advertising expenses as a percentage of revenue) for each company. The relationship was positive in half of the years and negative in the other half, but only to a limited degree, with correlations ranging from -0.3 to +0.3. In other words, changes in profit margins didn’t predict changes in advertising expense ratios in any consistent or meaningful way.

There are many reasons why the data might behave as it did in this study. To start, it’s important to note that there is a potential bias in the selection of companies included in my sample, which is not necessarily representative statistically, as it captures data from large advertisers who make relevant disclosures which are included in Refinitiv’s data sets. Moreover, any “perfect” analysis would ideally occur at the brand level rather than at the corporate level, and similarly would consider a range of profit-related metrics that vary by category and capture extended time horizons.

Putting those issues aside, there are many other factors which I think help explain advertising budget allocations better than profitability, however it might be defined.

While it’s undoubtedly true that in some categories budgets are determined based on performance-based metrics (which may be focused on improving profitability from a level which is being impacted by a wide range of other factors), my anecdotal observations of marketers have generally conveyed that they more often allocate spending on advertising based on rules-of-thumb around what they think the right level of spending is in a category for long-run growth. Others simply determine a future year’s budget by looking at the current year’s budget and tweaking it based on a wide range of alternative demands on corporate resources, although this similarly turns into a percentage of revenue-driven approach. In my simplified framework, changes in allocations are most likely to occur as the competitive intensity within a category waxes or wanes based on the emergence or disappearance of new competitors, which in turn could impact advertising expense ratios positive or negatively.

Source: Madison and Wall analysis of data for selected companies as aggregated by Refinitiv. Note that forecasts reflect sell-side analysts’ consensus estimates.