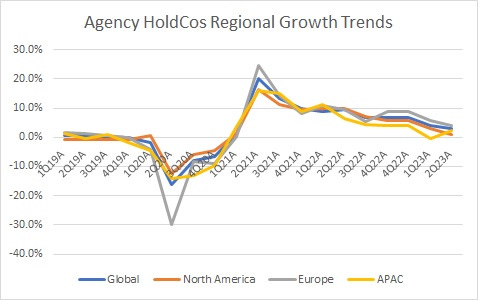

Large Agency HoldCos Grew ~3% Organically in 2Q23

With WPP reporting its second quarter 2023 results on Friday, we now have results in for the vast majority of the large global agency industry, including WPP, Publicis, Omnicom, Interpublic and Vivendi’s Havas. Although WPP reduced its guidance for the year, with organic growth shifting from a range of 3-5% to a range of 1.5% to 3%, the overall industry should still be positioned to grow within a 3-5% range.

Despite very difficult comparables – this group of five agency holding companies posted 9.6% organic growth in the second quarter of 2022 and 8.3% for the full year – second quarter growth amounted to 2.8%. Following on a 4.0% growth pace in the fourth quarter, I believe the industry remains on track towards a mid-single digit growth rate, made all the more likely with easier comparables from the second half of 2022 and improving sentiment towards advertising from the bulk of the industry (not to mention improving perceptions towards the US and global economies, where consensus is decidedly – if finally – moving away from a base-case assumption of a meaningful recession).

To be sure, WPP is now guiding towards a low digit growth rate as is Interpublic, but Omnicom and Publicis are likely to come in much closer to 5% (and probably above that level for Publicis), and as I have noted in recent research, independent mid-sized agencies have generally outperformed the broader sector, so would provide a boost to overall results.

By region, we can see that North America – where independent agencies are most pronounced, and where tech companies cutting spending were probably most pronounced, too – was the weakest region during the second quarter, rising only 0.8% for the five agency groups analyzed here. By contrast, Europe was a healthy 4.0%, and that’s despite strong 9.5% growth in the year-ago period. APAC remains relatively soft by comparison, growing by only 2.2% during the second quarter.

Source: Madison and Wall, Company Reports