Level-Setting Ad-Supported Streaming Share (But Emphasizing Critical Advantage Of Incremental Reach)

Streaming content is clearly growing in importance, and within it, ad-supported streaming is, too. However, exactly how much it is growing and what share it accounts for is sometimes difficult to assess, as headline data does not always capture the advertising industry’s reality as well as it could.

To make this assessment I’ve cut through data included in Nielsen’s monthly publication “The Gauge” as well as data on ad-supported subscribers to SVOD services from Antenna, and paired those data sets with a series of my own estimates to better mirror market shares as I think advertisers would define them when they manage their budgets.

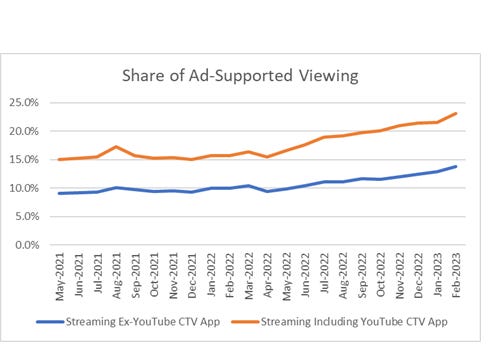

As a number I think we should focus on when looking at the share of ad-supported TV that ad-supported streaming accounts for, if we exclude YouTube’s connected TV app from a definition of TV viewing (as most TV advertisers would) I calculate that around 14% of ad-supported TV viewing occurs on ad-supported streaming content, up from around 9% of ad-supported TV viewing two years ago. If we include YouTube’s connected TV app as part of an ad-supported TV universe, the figures rise to 23% in the most recent data and under 15% around this time in 2021. By contrast, Nielsen’s headline figures suggest more like 40% of TV viewing occurs via streaming using one definition (including vMVPDs) or 34% using another definition.

Source: Madison and Wall, Nielsen, Antenna

There are several important and interesting issues to point to from this analysis.

The first is that there is, unsurprisingly, a meaningful volume of ad-supported streaming inventory, regardless of how it is defined, even if it is less than the headline data from Nielsen might suggest.

Second, there is a meaningful difference in the scale of streaming ad-supported inventory depending on whether or not YouTube’s CTV app is included. If it is excluded, CTV is sizeable, but still decidedly a minority of total TV viewing. Even if recent trends continue, ad-supported CTV viewing ex-YouTube will take many years before it is as big as ad-supported CTV including YouTube is today.

Returning to the gap between my estimates and the headline figures included in The Gauge, differences are primarily explained by the massive volumes of TV viewing that are not ad-supported. I estimate that this type of activity accounts for around 21% of all TV viewing, up from under 15% two years ago.

The growth of this viewing and its impact on campaign reach is most critical to monitor, especially for marketers who rely on ad-supported television today. To the extent that growing numbers of consumers may be mostly unreachable through ad-supported TV, marketers will need to reassess key elements of their media strategies. Including most of YouTube, TikTok and other forms of online video beyond the television set in a given marketer’s definition of television may be one approach, but another may be to focus instead on managing reach across multiple channels, or alternately revisit whether or not reach is even a metric to try and manage in favor of some other objective.

Consequently, in the near term what should matter to marketers much more than share of total time spent with each type of TV viewing are metrics such as unique reach or the percentage of people who spend more than a certain amount of time over a given period with different types of ad-supported TV. Ad-supported streaming services will almost certainly look more favorable on this basis when compared with the shares of viewing they represent, regardless of how ad-supported streaming is defined.