Media Company M&A: Catalysts and Consequences

Beginning in January 2024, most Madison and Wall research and related data published on this Substack will primarily be available to consulting or advisory clients, or otherwise as part of a paid corporate subscription. Please reach out to brian@madisonandwall.com if you would like to discuss these services or for more information about the new offering.

With news outlets building on Puck’s reporting last week regarding the potential for a transaction between Skydance, Redbird and Paramount’s controlling entity National Amusements, it’s a good reminder that regardless of whether or not anything happens between the aforementioned entities, a significant amount of M&A is likely to occur among today’s biggest traditional media companies in the foreseeable future. In this note I review the various shapes that M&A could take and the consequences on several different aspects of the business that may follow.

Beyond opportunistic scenarios such as the reported conversations involving Paramount, I can point to several specific near or mid-term events that could catalyze action for the industry:

In April, it will be two years since AT&T spun off Warner Media and combined it with Discovery to create Warner Bros. Discovery. As the transaction was structured as a Reverse Moris Trust, the entity needs to remain independent until the two year anniversary of its creation in order to avoid significant tax consequences

At Disney, CEO Bob Iger has been floating a wide range of scenarios for the future of Disney’s media businesses, including the sale of the broadcast network (or maybe just the stations) or maybe just selling several of its linear networks to A&E or selling stakes in ESPN to sports leagues. If there’s a near-term catalyst to point to, there will likely be meaningful cash requirements to pay its obligation to Comcast as part of the Hulu consolidation.

All of the larger network owners and smaller ones such as AMC Networks in the US and other comparably-sized (mostly) stand-alone global TV networks such as ITV in the UK, Pro7Sat1 in Germany and TF1 in France will all face new pressure as Amazon rolls out advertising to Prime Video subscribers by default early in 2024. Even though it’s unlikely to account for a massive share of spending, even a low single digit percentage of TV advertising budgets will be noticeable. Of course, this will build on the enhanced competition that Amazon, Netflix and Apple already provide for viewership and the relatively higher content costs that follow from their presence in the market for professional video content.

As was often highlighted in the press around Lachlan Murdoch’s transition to sole chairman of Fox, that company’s controlling entity, the Murdoch Family Trust, will eventually have to contemplate whether or not the Murdoch family controls the business, and if so, in what shape and with what assets.

What are the consequences of any transactions that might occur? Here are some to consider:

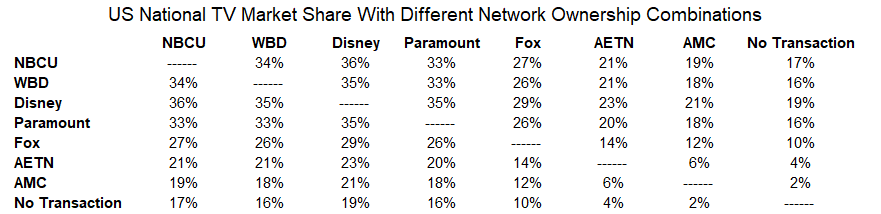

National TV ad sales as we currently define it would likely become more concentrated. In the case of Skydance and Paramount, it’s unlikely that they wouldn’t pursue an investment in a parent company without looking at consolidation – whether buying or selling – TV networks. With many national TV network owners concurrently owning local broadcasting businesses, it’s almost certain that local TV stations may need to be divested given FCC ownership caps which sit at 39% of US households. There is also currently a prohibition on a merger of any two of the four biggest broadcast networks, so it’s possible a broadcast network would need to be sold off separately or rule changes would need to be pursued, but then it’s also possible that an entity leading a transaction could still control the ad sales of a network subsequently disposed of. However it shakes out, the national TV advertising market share for the largest player could rise from close to 20% to more like 30%, and presumably subsequent transactions would lead to more concentration elsewhere. Should this matter to marketers, agencies, regulators or others? Twenty years ago, or even ten years ago, such concentration would have been meaningful and would have had a significant impact, but I doubt this would be the case now. Pricing power is not so much of a function of size or concentration but whether or not buyers have a credible ability to walk away, and marketers now have more-than credible abilities to walk away as they shift budgets towards digital media platforms. To put the point differently, the national TV market was much less concentrated a decade ago (prior to transactions including Disney’s acquisition of Fox’s cable networks, Viacom and CBS combining and Warner and Discovery coming together) when it was growing. Now that it is more concentrated, the industry’s ad revenues are in decline.

Source: Madison and Wall analysis of company reports based on estimates for 2022 national TV ad revenues. Shares assume combinations of all related businesses including streaming services.

Similarly, negotiations with cable operators probably wouldn’t be as impactful now as they would have been a decade ago. As we saw with this year’s Charter-Disney dispute, cable operators are mostly at or beyond a point of indifference in terms of providing better commercial terms to TV networks. It’s unlikley that any combination of TV network groups would have much more leverage.

There would be opportunities to cut costs because of duplication of operations, but presumably this would mostly serve to free up cashflow to fund streaming services (which are unlikely to be anywhere near as profitable as legacy businesses any year soon. Content costs might be better controlled when there are fewer bidders for content, all else equal, but relative to where the industry was ten years ago – prior to Netflix, Amazon and Apple becoming meaningful buyers of professional content – it’s probably not all that different in terms of the competitive environment for buying content now vs. the pre-streaming past.

Streaming services may benefit from effective “rebundlings” where multiple services might be combined for a discount to consumers, although I wonder if price points well in excess of $20 / month won’t lead to higher churn. If there is some optimal price point that limits churn and maximizes overall profitability, owners of streaming services might return to the idea of splitting up services rather than combining them as we are presently seeing (i.e. Disney+ and Hulu, Paramount+ and Showtime, Max and Discovery+, etc).

However, larger network groups would be far better positioned to compete with Netflix, Amazon and Apple with more scale in terms of maintaining access to capital vs. the status quo. The bigger and more practical issue as I see it relates to the pursuit of international scale. I would argue that the backing off of international expansion by several US network owners in the past year and a half was a missed opportunity from a longer-term perspective, effectively ensuring that the tech giants would take market share instead. To the extent that so many aspects of the business benefit from the pursuit of global scale, they would all be well-advised to invest more internationally. Moreover, I argue that one of the most important trends in advertising is that the globalization of tools, processes, measurement, etc. is one of the key factors helping the largest digital platforms to expand as they presently are. Everything involved with the pursuit of globalization by ad sales organizations helps to amortize costs and improve products (especially including those related to measurement).

Conversely, one or more of today’s tech-focused or retail-focused companies could decide that they would benefit from ownership of a traditional media business because of the immediate scale and institutional knowledge that would follow relative to building out such initiatves organically. Depending on who (i.e. an ad-focused or non ad-focused company) and the degree to which content or advertising inventory has synergies with an acquiror’s other businesses, the direction of the media industry could change, at least partially.

Since many possible combinations would require a divestiture of local TV stations, it’s likely that dispositions would occur. Because potential strategic buyers probably would be over the ownership cap if they were to buy a divested group, these entities might be spun out as independent entities (whether publicly or privately owned) following a transaction. What would then happen if ownership caps were eventually raised? At minimum I would expect that combinations would follow, which would likely focus more on cost cuts than anything more strategic. However, because these entities would have more scale, they would theoretically have greater opportunities to access capital and invest in entirely new directions. I’m doubtful it would make sense for new “broadcast networks” to get created, as revenue streams from advertising and subscriptions as they exist today would almost certainly be in a state of decline for incumbents, and newer players would struggle to take share.

The bigger opportunities for the industry are those which follow from the possibility of media companies reinventing themselves along the lines I’ve written about previously. Among other possibilities, those pathways might include combinations with or partnerships with mid-sized social media networks or more aggressive focus on subscription or direct-to-consumer-based revenue streams, and doing so at a global level as much as possible. The advantages of scale are real, but they may be offset if bureaucracy is more intense, or if the benefits of scale are used to return capital to shareholders rather than supporting the pursuit of opportunities wherever they may be.