Tech Advertising Category Analysis, Impact on Agency Revenues

With S4 Capital reporting results today featuring well-understood weakness in spending on advertising by marketers within the technology sector, I nonetheless received several questions today about related trends. Towards those ends, I thought it would be interesting to look at the relative scale of advertising activity from tech companies.

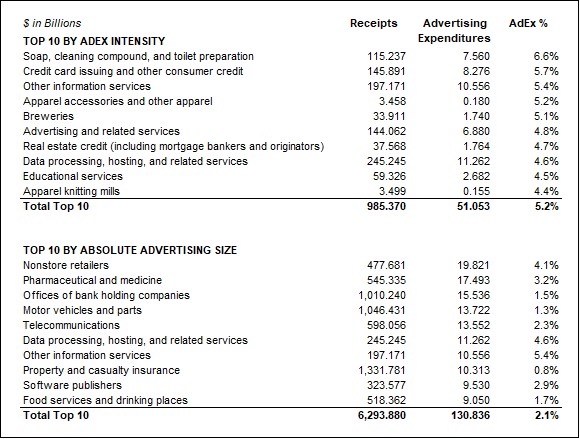

Using data for the United States from the IRS based upon samples of corporate tax returns for the most recent year available, 2019, we can see below how several of the top 10 categories fall within the broadly defined tech category, including information services, advertising and related services (i.e. media companies, mostly tech-based, advertising themselves) and data processing companies all among the top 10 in terms of intensity of spending with around 5% of revenues deployed into advertising (vs. economy-wide averages of 1.1%), which conceivably makes these companies appealing clients, especially considering their outsized revenue growth.

More significantly, if we look at the top 10 categories by total spending, groups which represent a third of all advertising, we can see how non-store retailers (i.e. e-commerce), telecommunications, data processing, other information services and software publishers are all technology categories which collectively represent a significant share of the industry – 17%, in total. Considering how the industry would have evolved over the course of the pandemic, it’s certainly a higher share now, at least in the US. Presumably shares are somewhat lower outside of the US.

Placing this back into context of the agency groups – and recognizing that there will be differences in definitions of categories and how many clients are included in these figures – it’s notable that during the most recently completed full year (2022) clients in the tech and telecom categories accounted for 14% of global revenue at Omnicom, 15% at Interpublic and 13% at Publicis. For WPP, tech, telecom and media clients accounted for 26% of revenue.

S4 is by far the stand-out in terms of category exposure, with technology clients alone accounting for 46% of revenue. To the extent that there is pullback in spending by this category, as has been widely reported and as is evident in the publicly disclosed numbers from many of the largest players in the sector, an outsized impact on companies so-exposed should be unsurprising - just as an outsized rebound may occur if spending trends normalize within the tech sector, presuming spending ratios as a percentage of advertising return to higher levels.

Source: Madison and Wall analysis of IRS data for 2019