3Q23 Agency Trends: Independents Flat, But Largest HoldCos Likely Poised To Grow By More

Beginning in January 2024, most Madison and Wall research and related data published on this Substack will primarily be available to consulting or advisory clients, or otherwise as part of a paid corporate subscription. Please reach out to brian@madisonandwall.com if you would like to discuss these services or for more information about the new offering.

—

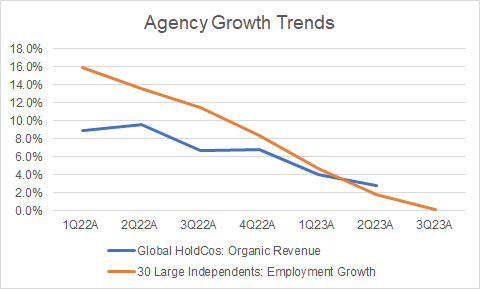

Independent agencies and smaller holding companies remain a fascinating space to study. These companies took market share from the largest holding companies in the 2010s and beyond the competitive trends they exhibit are important to monitor because they can be incubators for novel approaches to marketing and communications services.

To monitor independent agencies, I look at employment data from Linkedin (whose data I believe generally accurately reflects employment trends for individual companies in this sector) because in agencies, headcount growth is a proxy for revenue growth.

Looking at the latest data for a composite of 30 of the largest independents on a like-for-like basis (adjusting for acquisitions to make for a comparable base over all periods studied), we can see a continuation of the slowdown that has been occurring throughout 2022 and 2023, with essentially no growth for this group of companies in the third quarter of 2023 over the third quarter of 2022. Trends observed by tracking dozens of other, mostly smaller agencies shows very similar trends for the broader group as well.

Source: Madison and Wall analysis of company reports, Linkedin

In part I believe this slowdown can be attributed to difficult comparables (3Q22 growth exceeded 11%), but I suspect the same factors causing a slowdown for some larger agencies are at play as well: falling spending from technology firms. Although it mostly operates in an adjacent space, commentary from Accenture on its earnings call last week further validated the idea that technology firms are reducing their spending on outsourced services, with Accenture’s communications, media & technology clients cutting spending by -12% vs. an increase of +4% for the overall business during their most recent fiscal quarter ending in August (for their May quarter, the comparable figures were -8% and +5%). This follows on recent commentary from S4 Capital and Interpublic conveying similar trends for those agency groups.

Still, there are some stand-out independent agencies to point to. In particular, on the upside we can see high-single digit or double-digit growth from entities such as WebFX, PMG, ServicePlan, The Independents, Jung von Matt, Power Digital and the MARS Agency. By contrast, Tinuiti and WPromote appear to have experienced more than 10% declines. The relatively large DEPT. falling by 7% is also noteworthy. The mixed results of performance media agencies above (WebFX, PMG, Power Digital, Tinuiti and WPromote) suggests that client or sector-specific trends may be more at play than anything else. How much remains to be seen.

I note that earlier this year I incorrectly thought the easier comparables and a healthy overall economy and ad market should help support improving growth trends for the independents. Although economic conditions are still mostly positive, and my expectations for advertising is still to see stronger growth in the third quarter, it may very well be that the cuts we are seeing from tech companies could further erode growth for the largest agencies, too. On the other hand, the relatively easier comparables that large holdcos have from the year-ago period continues to suggest that they should have been able to fare better than the independents during the third quarter. We’ll know more in the next few weeks as their results come out.