US Audio Ad Revenues Fell -5% in 1Q23; Growth Needs To Emerge Beyond Advertising

Source: Madison and Wall, Company Reports

After last week’s review of current trends related to out-of-home advertising, this week I’m looking at the radio – or more accurately “audio” – advertising sector.

Audio advertising used to be significantly more important than it now is, at least as a business. In the United States, by far the biggest market for radio given its history focused on commercial rather than publicly-supported radio, at peak in the early 2000s, the medium generated more than $20 billion in revenue and would have accounted for a peak of more than 10% of all advertising, and significantly more if we only looked at locally-skewed advertisers. Fast forward 20 years and audio advertising in all of its forms accounts for around $16 billion, or around 5% of US advertising.

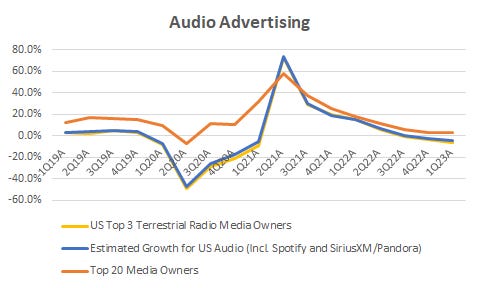

Looking at current growth trends during the first quarter of 2023, a review of the three largest terrestrial radio station owners in the United States (I Heart Media, Audacy and Cumulus) which account for around 40% of the sector show total ad revenues including digital properties (digital audio, podcasts, etc.) falling by around 6.1% on a pro forma basis excluding M&A and political advertising. This followed 3.3% growth for all of 2022, with the positive outcome primarily driven by the rapid growth observed across the industry during last year’s first quarter. By comparison, I calculate that the 20 largest sellers of all types of advertising (outside of China) grew by 3.2% during 1Q23 and by 9.0% during all of 2022.

If I appropriately weight this group of radio station owners and add the other two large pure-play sellers of audio inventory, SiriusXM (which also owns Pandora) and Spotify, with an assumption around Spotify’s US revenue skew, I calculate a 4.9% decline for all audio advertising during the first quarter of 2023 following on a 4.0% gain during 2022. Presumably the numbers would look a little bit better if the podcast divisions of companies not primarily focused on audio (such Amazon) were added, but not by much, as those businesses are small in absolute terms. While it’s possible that difficult comparables are a factor, unlike TV and digital media, which also faced similar challenges in the first quarter of 2023, audio advertising has yet to exceed pre-pandemic levels on a full year basis.

I think that the absence of a complete recovery for audio advertising is significant, if unsurprising to me.

For a sense of where the business is vs. its pre-pandemic peak, I estimate that on a pro forma basis, the three biggest US radio station owners were 8% smaller in 2022 relative to 2019, and I estimate that the overall audio advertising sector including Spotify and SiriusXM was around 3% smaller in 2022 vs. 2019. A brief review of some of the larger international radio groups shows much bigger gaps, incidentally. Canada’s Corus did grow its radio division during the most recent quarter, but its revenue base was approximately 28% lower during calendar 2022 relative to calendar 2019 levels. In France, a composite of NRJ and M6’s radio stations shows a pair of businesses that were 21% smaller in 2022 vs. 2019. Meanwhile, Australia’s Southern Cross’ advertising revenues were 12% smaller in 2022 than they were in 2019.

I am doubtful that US audio advertising will ever exceed its pre-pandemic levels. Ongoing decline seems more likely, despite operating as part of a broader advertising industry that should return to mid-single digit growth trajectory beyond this year.

This can be true despite a myriad of positive attributes for audio. It has superior levels of reach vs. other media, accounts for significant volumes of time spent and should benefit from research that can show the medium to be highly effective and efficient. However, I argue none of this matters as much as the factors which I think are responsible for the medium’s relative decline over the past couple of decades.

First, larger regionally-constrained businesses have generally become national in terms of their footprints, and their media and marketing activities have followed suit. This predisposes those nationally-skewed advertisers to use media which are consistently available across a given country, and second causes those advertisers to assess a different range of choices (i.e. local TV might be viewed as expensive to a locally skewed advertiser, making local radio relatively more appealing, but national TV might be viewed as inexpensive on a relative basis, making national radio relatively less appealing by comparison)

Second, it’s increasingly possible for smaller businesses to operate at a national or global level than might have been true in a pre-internet era. This similarly causes marketing choices to shift towards those media which are comparably organized.

And third, since the self-service advertising took off with search in the early 2000s, smaller businesses have found they can more readily use digital platforms at any price point, whether spending $100 per month or $100,000 per month, providing a high degree of incumbency that can be difficult for other media to overcome, at least until those marketers are mature enough to explore the benefits of diversifying their media mixes.

However, none of this means the owners of legacy audio businesses are necessarily pre-disposed to decline in total:

As historical owners of radio continue to invest in their digital platforms, they are evolving their businesses to better match advertisers’ increasingly national skew. That will help to offset some of the decline of the traditional business.

Next, most of those same owners will continue to find ways to demonstrate the cost-effectiveness of traditional radio to larger advertisers, which will probably help to overcome some of the structural limitations described above, and that will likely contribute some incremental revenue as well.

Another source of growth may come as if owners of audio properties scale up additional services for the marketers they can super-serve (this already occurs to a modest degree as with local promotions or events that radio owners develop).

The development of other consumer-centric and consumer-paid services may provide another pathway to growth, especially as there is so much demand for two of the main types of content traditional radio historically provided. Spotify, Amazon, Apple and Google have each demonstrated that consumers are willing to pay for access to music services. Publishers such as the New York Times, News Corp and others continue to demonstrate that there is a willingness to pay for news content, too.

My own experience in community radio in the 1990s showed me that audio can be a vibrant medium, even when it’s not much of a business, if only because content doesn’t need to be expensively produced to be highly desired by an audience. Regardless of the state of the business in years ahead, audio platforms will still retain much of their importance as a result.